While AI and automation were front and centre, the real conversations happening in the room were about much deeper issues: trust, adoption, interoperability, and value. It wasn’t about showcasing tech for the sake of it - it was about what’s actually working, and what’s still holding us back.

Here are some of the biggest takeaways:

1. We’re drowning in data, but still hungry for the right insight

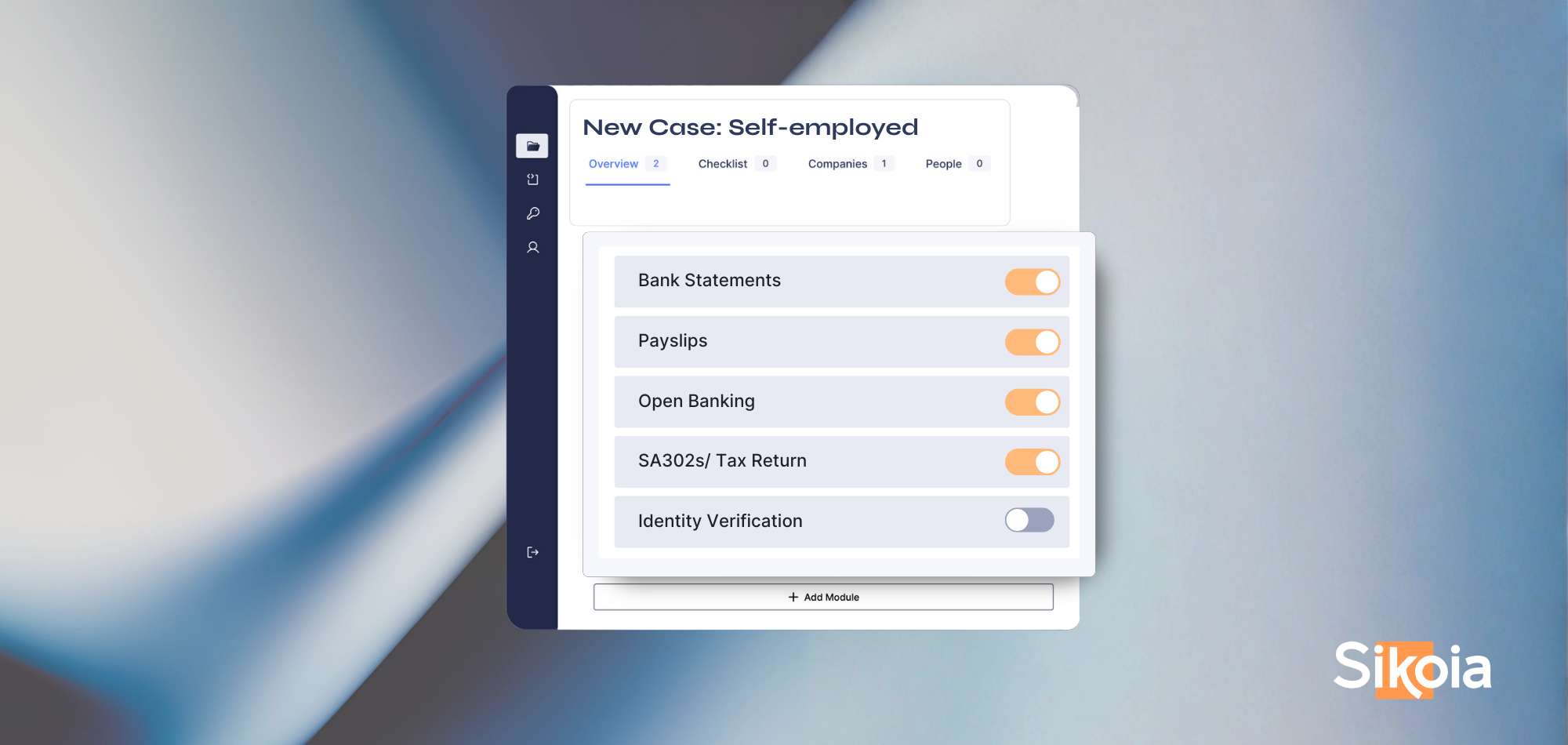

Every stage of the mortgage journey from KYC to affordability is riddled with redundant, repetitive data gathering. And yet, key decisions still rely on PDFs, emails, or manual processing. A recent FCA report put the cost of a single affordability check at £31 per applicant, underscoring just how expensive inefficiency has become.

Platforms that can intelligently structure and surface relevant data, whether via AI, orchestration layers, or verified third-party sources are no longer nice-to-haves. They’re foundational to improving economics and customer experience.

2. AI isn’t a feature. It’s a tool, if you know where to use it

AI can’t replace brokers, advisers, or underwriters and it shouldn’t. But it can make them better at what they do. Particularly in areas like document classification, fraud flagging, and income verification, AI shines when it’s used to reduce friction, not decision rights.

One panellist put it simply: “If AI doesn't speed things up or make things clearer - it’s just noise.”

3. The bottleneck isn’t tech. It’s integration

Tech overload and fragmented systems remain one of the biggest blockers to innovation. Advisers often juggle tools that don’t speak to each other, and lenders are wary of introducing another point solution that creates more manual work.

The real innovation lies in building more connected, flexible infrastructures - whether via orchestration layers, smarter APIs, or partnerships that surface verified data in the same user journey. It’s not about adding more, it’s about making what we have work together.

4. Ecosystem players must act as enablers, not gatekeepers

Innovation doesn’t scale in isolation. What stood out across the conversations was the need for collaborative, modular innovation - giving lenders, brokers, and platforms the flexibility to choose their own tools but still get to the same output.

That principle is at the core of Sikoia’s vision. By embedding Sikoia’s AI capabilities into internal systems, external CRMs, loan origination platforms, or credit bureaus, users can build fully native, AI-powered workflows with minimal process changes, high user adoption, and near-total case coverage.

5. Adoption isn’t about features. It’s about outcomes

No matter how powerful a platform is, if it can’t demonstrate measurable uplift in speed, accuracy, or conversion - it won’t scale. As several panellists shared, budget constraints mean 80% of tech spend still goes to maintaining legacy systems. That remaining 20% must earn its place.

Successful rollouts are the ones that:

- Improved hit rates or submission quality

- Reduced adviser support queries

- Give lenders earlier confidence on affordability

Where we go from here

Innovation in mortgage tech isn't about who has the most features. It’s about solving the right problems: data duplication, disconnected journeys, lack of clarity for customers, and time-consuming affordability checks.

AI and Open Banking will absolutely have a role to play but only when the use case is clear, the value is shared across the chain, and the user experience is better than the status quo.

We're grateful to everyone who contributed to the event for the candour, curiosity, and challenge.

If you'd like to explore how these topics play out in your own processes, please book an intro call and we'd love to continue the conversation. Book an intro meeting here.

.png)

.png)

.png)

.png)

.png)

%20(2).svg)