With the deadline for the Consumer Duty rapidly approaching, the Financial Conduct Authority (FCA) has called on financial service providers to ensure they are prepared to meet the new requirements. A recent survey by Consultancy Bovill revealed that nearly half are uncertain about the time needed to implement this regulation - as is to be expected with a new suite of regulatory requirements. But a deeper look at some of the implications and consequences suggests that the providers who adapt best will thrive.

In this blog, we explore the impact of Consumer Duty on financial services, highlighting its key outcomes and outlining ways firms can adopt a customer-centric approach to drive their success.

Understanding Consumer Duty

The Consumer Duty is a new FCA obligation that applies to any firm involved in determining outcomes for retail customers, including SME customers. Its overarching goal is to promote positive customer experiences, protect consumers from financial harm, and enhance the competitiveness of the financial services sector. The Consumer Duty is defined by four key outcomes that financial service providers must adhere to:

- Products and services: The Consumer Duty ensures that products and services are customer-centric and distributed in line with consumer interests.

- Price and value: The Consumer Duty enforces fair pricing practices and transparent disclosure of costs, fees, and charges, delivering valuable products and services to customers.

- Consumer understanding: Firms must communicate with customers using clear language and formats to enable informed decision-making about financial products and services.

- Consumer support: Firms are obliged to offer prompt and reliable customer support, ensuring accessible channels for addressing queries and concerns.

Challenges and Opportunities

The Consumer Duty brings a wave of regulatory changes, representing both a challenge and an opportunity for financial service providers. Some have expressed concerns over the additional administrative and operational burdens that the regulation may impose, particularly for companies already operating on tight margins. However, if implemented correctly, the Consumer Duty can prove beneficial for firms in multiple ways.

- Customer retention and attraction: By placing customer interests at the forefront, firms can enhance their reputation and build trust with consumers. This, in turn, can lead to increased customer loyalty and the attraction of new customers who value transparency and fair treatment.

- Competitive advantage: Embracing the Consumer Duty can give firms a competitive edge. Those who prioritise customer-centricity and consistently deliver positive outcomes are likely to stand out from their peers, making them more appealing to consumers.

“The FCA expects companies to monitor, regularly review and assess for risks to good consumer outcomes. This requires extensive data collection, customer research and analysis.”

Adopting a Customer-Centric Approach

To effectively navigate the Consumer Duty and harness its potential benefits, financial service providers must adopt an "outside-in" approach that revolves around customer experiences and needs. This means consistently evaluating customer feedback and insights to shape products and services. Here are some key steps for success:

- Customer-centric mindset: Firms should genuinely understand and empathise with their customers' perspectives. This requires standing in their shoes and continuously scrutinising customer experiences and outcomes to identify areas for improvement.

- Actionable insights: Gathering extensive data, conducting customer research, and performing thorough analysis are critical to identifying trends, pain points, and opportunities for enhancing customer outcomes. These insights should guide decision-making processes.

- Holistic approach: Rather than relying solely on off-the-shelf solutions and technology platforms, providers should start with well-informed hypotheses grounded in customer understanding. This approach ensures that changes made align with customer needs and aspirations.

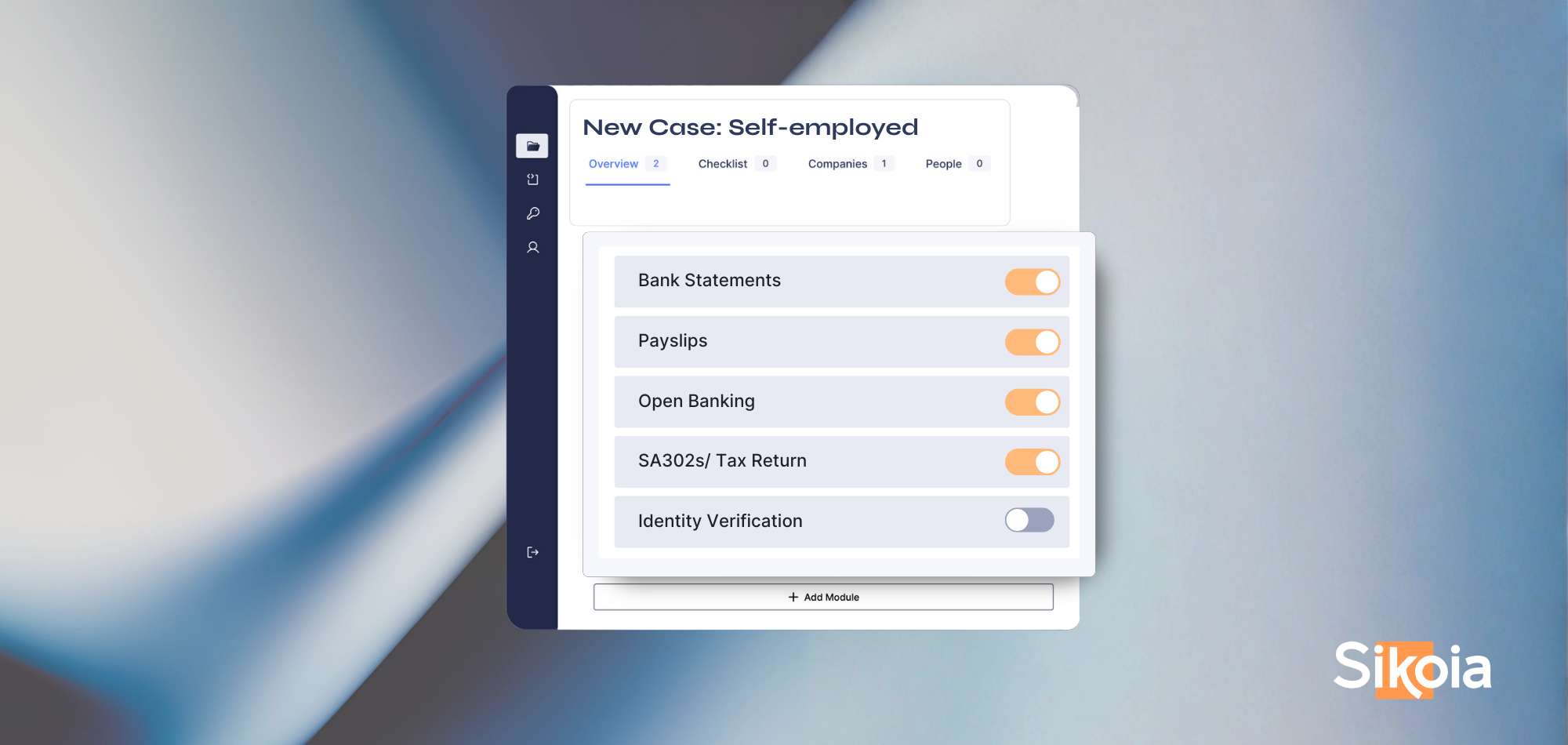

At Sikoia, we think one of the easiest ways financial service providers can be ready to succeed in this new environment is by deeply embedding a unified approach to data into their systems and processes. By bringing all your customer financial and identity data together in a single layer, it becomes easier to surface meaningful, customer-centric insights – and easier to embed these into all your customer touchpoints.

.png)

.png)

.png)

.png)

.png)

%20(2).svg)