In a mortgage market where nobody is quite sure what is going to happen next, it is crucial that lenders get better insights into their customers’ finances. Current affordability assessments have failed to adapt to dramatic changes in the economy and are no longer fit for purpose.

Why is affordability important to mortgage lenders?

Lending money to people who cannot afford to repay it is a mistake that mortgage lenders, who are highly regulated and rely on interest and investment to make a profit, do not want to make. The Financial Conduct Authority (FCA) is the regulatory body responsible for lenders in the UK and has strict guidelines that all of them are required to adhere to by law.

The FCA has implemented the principle of Consumer Duty, which is aimed at improving outcomes for consumers. Under the Consumer Duty, lenders must act in good faith towards customers, avoid causing them harm, and enable and support them to pursue their financial objectives. Consumers should receive products and services that meet their needs at fair value, communications they can understand, and customer support when required.

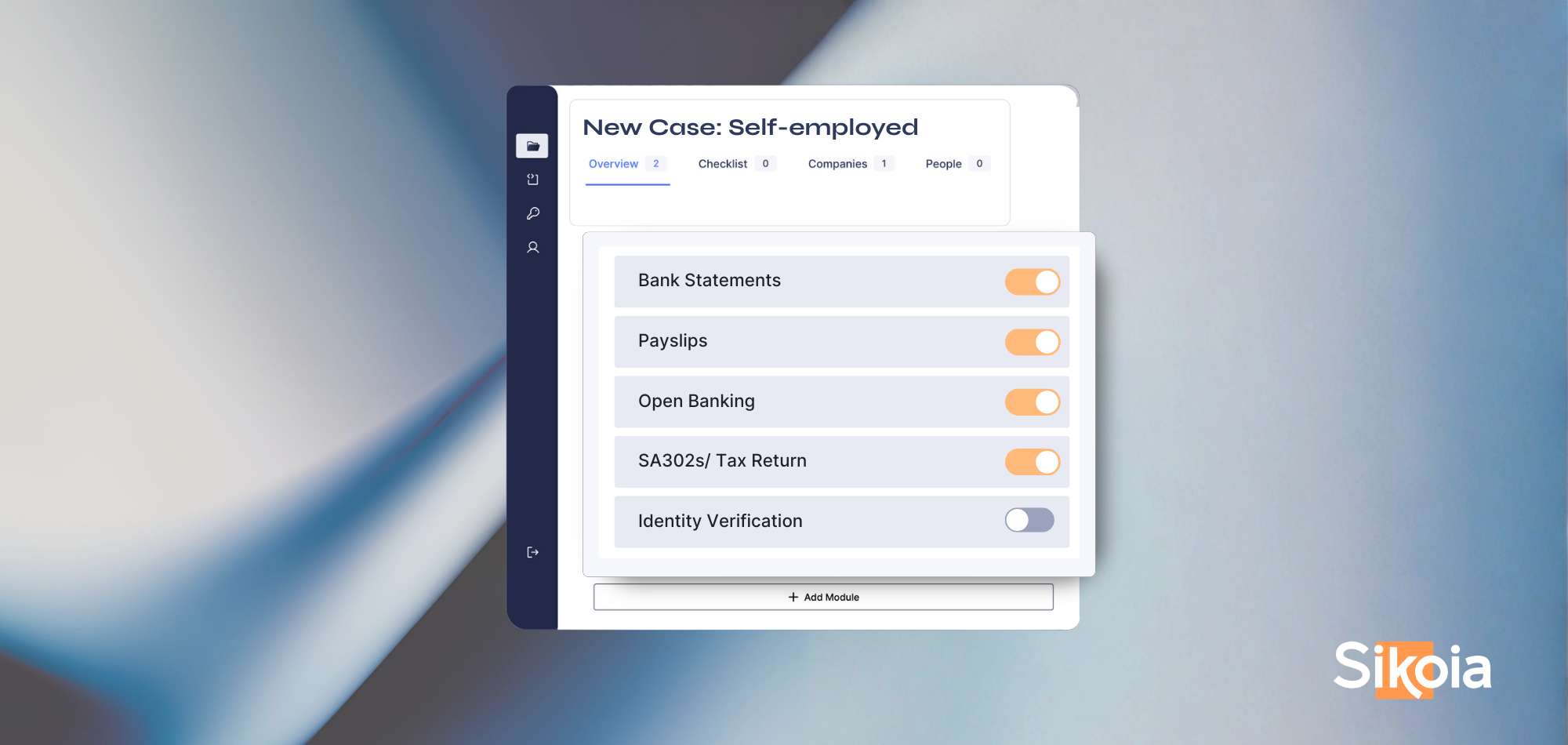

A key element of the FCA guidelines involves conducting customer affordability assessments. These assessments are crucial for determining the appropriate loan amounts for customers, if any. As an integral component of consumer protection, they aim to prevent customers from borrowing more than they can afford to repay, thereby reducing the risk of financial difficulties. During an affordability check, lenders meticulously consider several factors:

- Income and expenses

- Credit history

- Debt-to-income ratio

- Financial dependencies

It is crucial that lenders fully understand whether customers can afford to repay their mortgages because lenders can end up in trouble with the FCA if they do not abide by regulations.

Mortgage lenders are struggling with affordability

Mortgage lenders in the UK are tightening their eligibility criteria amid the cost-of-living crisis. Experian saw demand for its analytics-driven data increase over 2023 because lenders are looking to monitor their potential (and existing) customers’ finances more closely. This is illustrative of the point that lenders are struggling to assess customer affordability in today’s unstable mortgage market.

Consumers have experienced interest rate shock as well as the rising cost of living. Uncertainty and insecurity are causing people’s financial situations to fluctuate. The lack of stability makes it more crucial for mortgage lenders to conduct accurate affordability assessments on customers; they need to mitigate very real risks. Unfortunately, instability also makes it harder for them to do this.

Changes in the economy

Changes in the economy have had a huge effect on today’s mortgage market and people’s personal finances. Two key factors make it harder for lenders to assess affordability: interest rates and the rise in living costs.

1. Interest Rates

Many people are struggling with their mortgage repayments after Liz Truss’ Autumn 2022 Mini Budget caused the pound to crash and interest rates to sky-rocket. In a single week, the average two-year fixed rate rose by 0.45%. Looking at interest rates through a slightly wider lens shows just how much they have soared over time. The average two-year fixed deal increased from 2.34% in December 2021 to 6.05% in November 2023.

People are spending more money on their housing costs each month. They have less cushion between the top end of what they can afford and how much they are actually paying, so are more likely to struggle with repayments. Since interest rates are linked to the Bank of England base rate, we need inflation to decline in order for interest rates to stabilise properly. Otherwise, people will continue to struggle.

2. Rise in Living Costs

The cost of living has increased, with the average household seeing energy bills set to rise by nearly £100 in January 2024. The average cost of supermarket items also increased by 25% between the summers of 2021 and 2023. To put it bluntly, most households are stretched. There is only so much cost-cutting people can do on essentials. They are less able to afford increased mortgage payments alongside the rise in living costs.

How are affordability assessments affected?

Changes in people’s personal finances have significantly impacted the accuracy of affordability assessments. It is harder for lenders to get a holistic view of their customers’ financial situations when both personal finances and wider economic factors are shifting. Lenders are finding it more difficult to determine whether their customers can actually afford their mortgage repayments.

The old models no longer work

The economy has changed. It is clear that the old models are no longer sufficient and affordability checks need improvement. Mortgage lenders currently pull data from varied sources in different ways. This data is highly useful in giving snapshots of customers’ finances. However, it often has to be manually sifted and analysed in a time-consuming way, leaving too much room for human error.

Affordability assessments need to look at customers’ financial situations as a whole in order to give lenders a much more accurate view of the risks. The industry is making great technological advancements in many aspects of finance, but how we measure affordability is still behind the curve.

What is the solution?

Automating data extraction from core financial documents, including bank statements and payslips, is a great first step. It saves time and eliminates human error. The next step is to automate collating and viewing this data. A holistic view of customer finances is needed to accurately assess affordability. Presenting the data in a consistent, digital format lessens the likelihood of human bias dictating varied outcomes, depending on which underwriter is assessing it.

Mortgage lenders need affordability assessment solutions that provide comprehensive overviews of their customers finances, eliminate bias and error and save them valuable time. The solution is to automate the data extraction process and compile the data in a harmonious way. Only with an accurate picture of their customers’ finances can lenders adapt more readily to dramatic changes in the economy.

.png)

.png)

.png)

.png)

.png)

%20(2).svg)