The FCA estimates that each affordability check costs lenders an average of £31.90 in staff time, and consumers approximately £21.90, driven by document-gathering, form-filling, and back-and-forth with brokers or administrators. In high-volume lending environments, this translates to millions of pounds annually in operational overhead.

The consultation proposes two major changes to how affordability can be assessed in specific scenarios:

- Expanding the use of Modified Affordability Assessments (MAAs), allowing borrowers to remortgage to a cheaper deal with a new lender even if a traditional full affordability check might have blocked the move.

- Simplifying the requirement for a full affordability assessment when reducing the mortgage term and remortgaging, provided the lender adheres to its Consumer Duty and responsible lending obligations.

These changes are designed to unlock flexibility for borrowers and efficiency for lenders, while maintaining appropriate consumer protections.

Why this matters for lenders and brokers

The FCA is signalling a more proportionate and outcomes-based approach to affordability. Rather than requiring a full manual review for every change, the focus is shifting to risk-sensitive assessments that reflect the nature of the transaction and the customer’s needs.

But with this flexibility comes responsibility. Lenders still need to ensure that affordability checks are accurate, documented, and compliant with the Consumer Duty, and that customers are not exposed to foreseeable harm.

The problem with traditional affordability checks

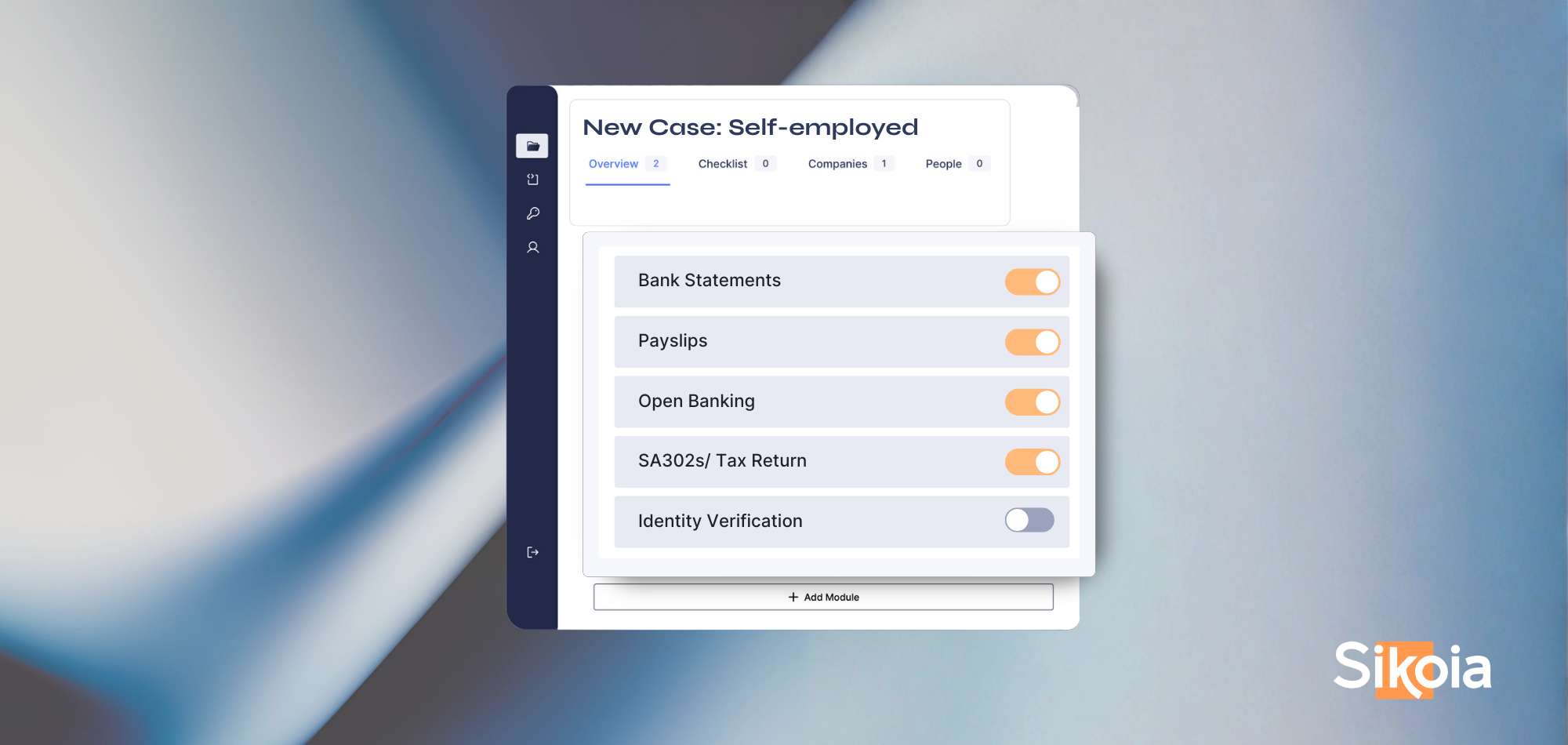

Whether for a remortgage or a term change, assessing affordability often requires a case-by-case manual review of documents such as payslips, bank statements, and tax returns. These steps are resource intensive, prone to delays, and frustrating for both customers and operations teams.

Even with the FCA proposing a more flexible, risk-sensitive approach to affordability assessments, firms are still expected to meet their obligations under the Consumer Duty. That means ensuring checks are not just fast, but also accurate, traceable, and fair.

Automating for speed, accuracy, and scale

Sikoia’s Document Processing solution uses intelligent automation to extract, validate, and standardise customer data from a wide range of unstructured documents. This eliminates the need for manual reviews and enables underwriters to focus only on cases that require deeper scrutiny.

The benefits are substantial:

- Faster turnaround times and real-time feedback for customers

- Reduced operational workload across compliance, credit, and ops teams

- Fewer errors and greater auditability for regulatory assurance

- Significant cost savings and improved process efficiency

Across large mortgage books, this can unlock millions in productivity gains every year.

A timely opportunity for transformation

The FCA's paper signals a broader shift towards efficiency and customer-centricity in mortgage regulation. For institutions looking to modernise their affordability processes, the timing could not be better. By embracing solutions like Sikoia’s Document Processing, lenders can reduce cost, improve compliance, and deliver the kind of seamless experience that both customers and regulators now expect. Now is the time to review your affordability workflows and consider how automation can support your transformation goals.

.png)

.png)

.png)

.png)

.png)

%20(2).svg)