Open Banking was hailed as the future of finance because it enables financial data to be shared quickly, easily and securely. You would expect mortgage lenders to take advantage of this. However, only two mortgage lenders accept Open Banking: the rest require traditional offline evidence, such as copies of payslips, tax returns, or bank statements. So does Open Banking really move the needle?

What is Open Banking?

Open Banking enables consumers to share their banking data with businesses or organisations who are not their bank. In the UK this is limited to companies who are directly enrolled in the Open Banking Directory and authorised by the Financial Conduct Authority (FCA) or a European equivalent.

Consumers’ financial data is shared securely and only with their explicit permission, typically via an online consent mechanism. The company then gets access to the consumer’s banking information in a one-time data exchange.

Do People Use Open Banking?

Open Banking is a relatively new concept; the legislation that mandated its adoption by the CMA 9, the second Payment Services Directive, only came into effect in early 2018; and roughly 2.5 million businesses and consumers have used Open Banking facilitated products since then. While this seems significant, for context there were around 45 million adults living in England in 2022, so it only accounts for a small proportion of the total number of potential customers.

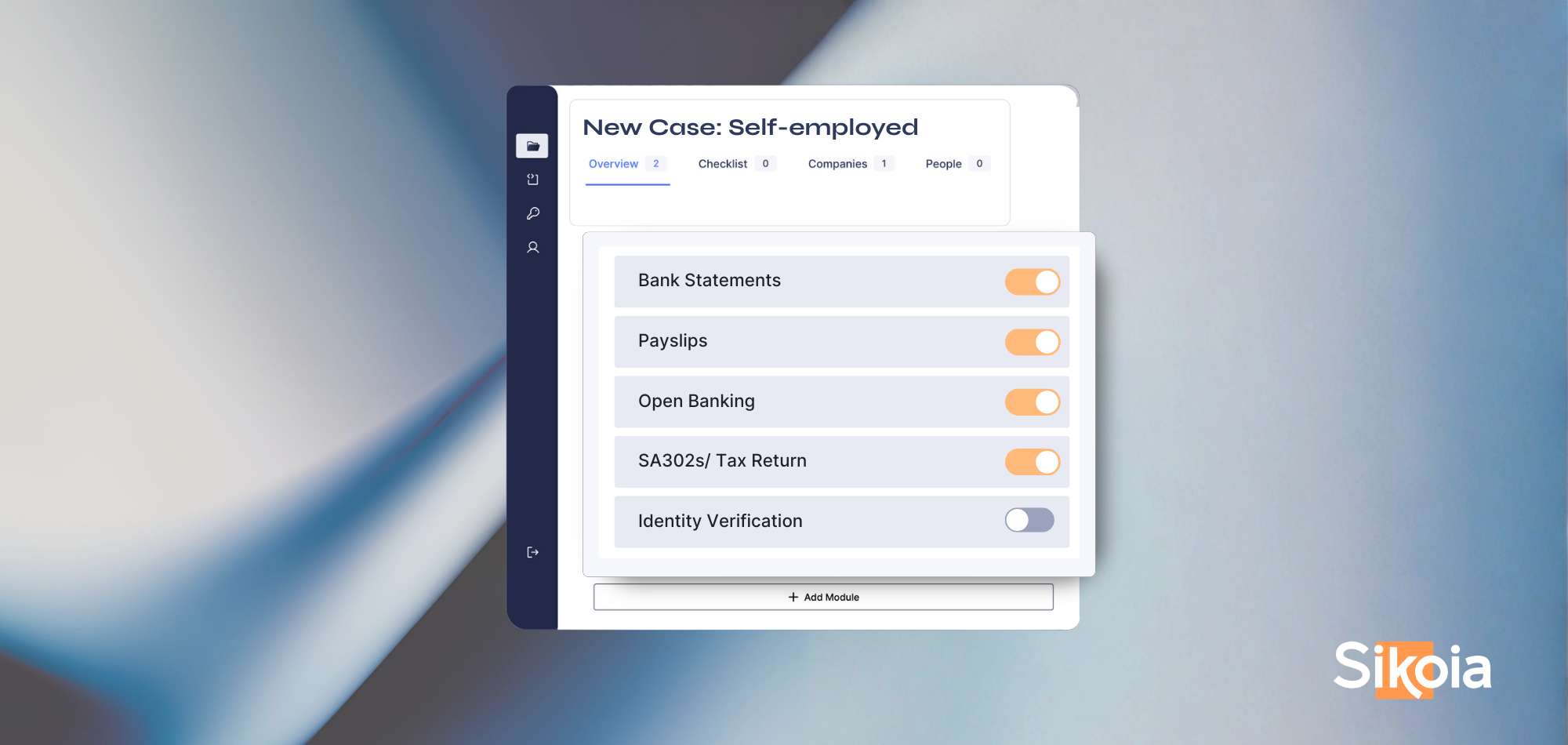

Mortgage lenders are a primary example of companies who could benefit from Open Banking. Customers previously had to download and share their bank statements to support a mortgage application, potentially repeating the process if they made a mistake or more data was needed. In theory, Open Banking allows the consumer to simply tick a box and allow the lender to source whatever information they need from their banking history. In reality, take-up of Open Banking has been slow in the mortgage industry: only two lenders accept it as of 2023 and most brokers report uptake well below 10%.

In order to figure out why usage is so low, it is important to weigh-up the benefits and limitations of Open Banking.

Benefits of Open Banking

- Digital process: Open Banking digitises the entire process of sharing financial information, making it quicker for consumers to share their bank data with companies. There is no longer any risk of them providing a lender with the incorrect information, for example, misunderstanding how many statements they need for a mortgage application, because the lender can access all their bank data at once.

- Up-to-date information: Lenders receive a more up-to-date view of their customers’ finances because Open Banking gives them access to their customer’s current banking data. Having up-to-date information may help them more accurately assess how much they can lend the customer and at what interest rate.

- Efficient payments: Lenders can request payment directly from a customer’s bank account (with consent), speeding up the repayment and collection process. A faster process likewise provides a more efficient payment experience for customers.

Limitations of Open Banking

- Low consumer uptake: Five years on from its implementation, and 64% of people in the UK have still not use Open Banking. They are more likely to opt for the more familiar option of bank statements when offered a choice. If Open Banking offers comprehensive benefits to both lenders and consumers, why is it not more widely used?

- Lack of standardisation: Open Banking as currently implemented is not standardised across the financial industry, as shown by the variation in lookback windows at different banks and building societies. Within the same bank, lookback windows vary between Account Information Service Providers – and customers have no control over this. Open Banking may cause them to over-share data that is not needed but which could decrease their chances of being approved for a mortgage. They are understandably reluctant to do this This is problematic because it can cause varied outcomes for the same customer applying for similar products. Customers can become dissatisfied with and distrustful of lenders when they feel like they are not being treated fairly.

- Fear of data misuse: Customers are also scared of data misuse, with only 16 percent of them believing Open Banking is safe. Data breaches are a popular topic in the media and with 60 percent of people still unsure about how Open Banking works, it is natural for them to mistrust it. Combined with the risks of oversharing, it’s unsurprising that mortgage advisers steer their customers away from Open Banking. Limited data: Open Banking also gives lenders less actionable data than hard-copy bank statements. For example, customer addresses aren’t part of the specification, so lenders cannot complete a proof of address check. Instead, customers have to share an alternative proof.

- Lack of customer engagement: Open Banking lessens the need for contact between lender and customer. This lack of personal relationship means the lender has fewer opportunities to build trust and understand their customers unique needs, making it harder to build long-lasting relationships.

Bridging the Gap

While Open Banking has been a significant step forward for the industry, and represents a significant shift in philosophy and approach, its current rollout is insufficient. Without changes to address the limitations above, bank statements will continue to be a crucial part of the mortgage application process. So how can lenders and intermediaries start optimising this manual process?

Our Affordability Insights solution plays an important role in bridging this gap: it quickly and automatically derives sophisticated analyses from bank statements and Open Banking alike, and allows lenders and intermediaries to deliver a standardised mortgage application experience.

Of course, bank statements are just one document type that lenders may need: for self-employed customers, lenders often need tax returns or other financial documents as well; and in less complex scenarios, payslips may be important. For all that Open Banking has transformed the industry, it’s clear that it isn’t yet the silver bullet the mortgage industry had hoped.

.png)

.png)

.png)

.png)

.png)

%20(2).svg)