One of the biggest challenges facing payment providers today is the need to implement effective KYC (Know Your Customer) processes, whether on businesses or consumers. However, for many providers, KYC procedures remain problematic: too often, providers struggle with manual and error-prone processes, have to work around gaps in the availability of public data, and find it difficult to accurately identify ultimate beneficial owners (UBOs). To complicate things further, regulatory requirements are constantly shifting. Fortunately, by adapting their processes and technology, payment providers can successfully navigate these challenges and emerge as competitive leaders in the industry.

Current processes are manual and hard to report on, resulting in false positives and potential fines

Processes that are either manual or semi-manual are slower and more susceptible to errors. KYC specialists often spend too much time simply reconciling data across each case, with no easy way of being able to prioritise the more complex ones. With so much manual intervention, simply keeping track of everything is complicated, especially capturing evidence for your reporting obligations.

Adding to this, payment providers must constantly adapt their processes to stay compliant as risk criteria and regulatory requirements evolve. This is even more true in “B2B” scenarios: collecting international ownership data is challenging, requiring payment providers to navigate different legal systems and cultural conventions, which can lead to delays and errors in the verification process.

Data collection is scattered and incomplete

The lack of reliable public data makes it difficult for payment providers to verify the identity of customers, particularly in regions that are not as digitised as the UK. Often providers may have to deal with completely different rules on UBO identification, as well as differing regulatory requirements and conventions. In some regions, processes may be almost entirely manual and document-driven, whereas others have an expectation that everything can – and should – be done digitally, causing difficulties for both compliance teams and customer support teams.

Rapidly changing regulatory landscape

The changing regulatory landscape, including increased scrutiny from regulatory bodies like the Financial Conduct Authority (FCA), requires payment providers to stay up –to date with the latest regulatory requirements and adjust their processes and tech stack accordingly. This can be challenging, particularly for smaller payment providers who may not have the resources to do so. Moreover, the penalties for getting it wrong can be severe – after all, providers may literally be at risk of abetting international money laundering.

Adapting processes and technology to navigate the challenges

As we’ve previously discussed, there are immediate benefits of switching to an automated approach to KYC – especially when it comes to supporting quicker times-to-decision and enforcing policy compliance. These are particularly valuable in the competitive payments space. But to support this, you need a unified approach to your data and policies.

A Unified Data Platform (UDP) will help automate much of your KYC process, making it faster, more accurate, and more reliable. By unifying and normalising public and private databases, as well as social media and other online sources, UDPs provide standardised access to all your customer data, making it easier to verify the identity of customers more quickly and more accurately, regardless of the underlying complexity in gathering the data.

By leveraging these advantages, businesses can differentiate themselves and stay ahead in a dynamic market.

How can we help you?

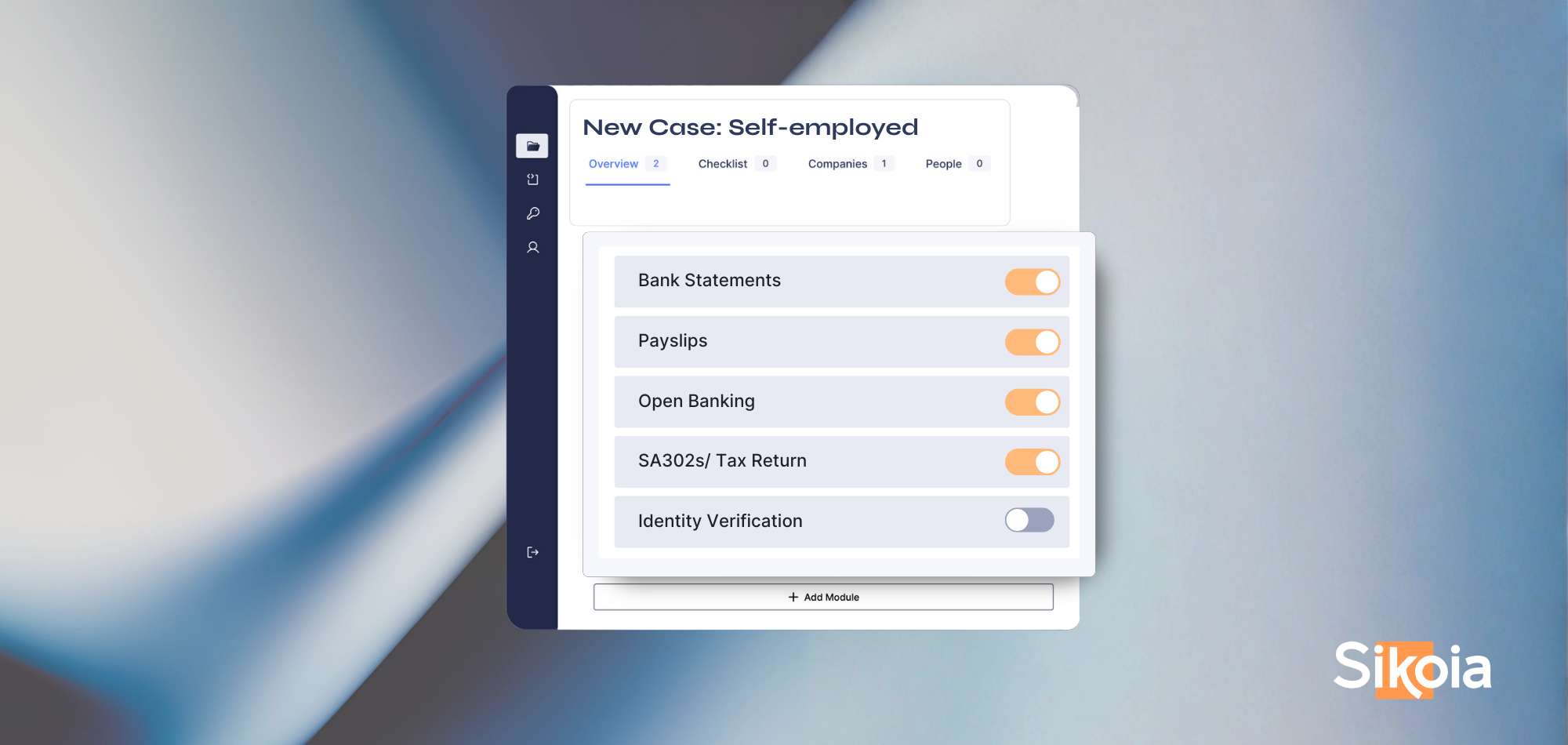

Sikoia’s Unified Data Platform allows financial service companies to conduct thorough customer due diligence – and support their reporting obligations in one single customer view with no need to negotiate multiple vendor contracts, all with its proprietary tech.

Sikoia’s Unified Data Platform centralises client financial and identity data to simplify onboarding and verification, monitoring, and risk evaluation. Sikoia’s UDP includes access to a growing marketplace of international data partners and compliance services, including credit bureaus, public registries, identity verification, fraud screening, AML screening, and more. This makes it easier to verify the identity of customers, especially in regions where public data is incomplete or unreliable. In today's world, where cyberattacks and identity thefts are on the rise, having a reliable and robust KYC process is more important than ever.

Ready to dive deeper? Schedule a meeting with me to explore the insights from this blog post. Simply click here to book your session!

.png)

.png)

.png)

.png)

.png)

%20(2).svg)