As we have previously discussed, the key to turning your formal compliance and risk assessments into a competitive advantage is your customer data: the data you have, the way you use it, and the value you can therefore extract from it. Many of these new APIs have an important role for companies looking to make a credit decision – in fact, all the capabilities and data sources that a company might need to start extending financial products can be accessed and integrated programmatically.

“Every company will be a fintech company”

As a company that helps businesses manage this ecosystem of providers, we’ve seen several waves of new capabilities emerge. For companies who are looking to introduce new financial products, whether they are lenders and intermediaries in a traditional space such as mortgages, or an online marketplace looking to introduce an embedded finance product, or even a retailer launching a buy-now-pay-later offering: the data and functionality needed to launch any of these products is accessible via an API. Examples include:

- Digital ID verification

- Accounting data access

- Payroll data access

- Government data access

- And, of course, Open Banking

Open Banking: the flagship financial API

Open Banking is poised to reshape the financial industry. It provides third-party financial service providers access to a goldmine of financial data using the latest APIs. Many fintechs are taking advantage of this innovation to create entirely new categories of financial products for consumers and small businesses. For instance, you may already be using a personal finance management app right now that leverages the power of Open Banking to provide insight across all your accounts in a single place.

The payment functionality that Open Banking supports is transformative in itself, and we can expect to see more and more ecommerce sites using it as a payment option in the future. But it’s as a data source that you’ll find Open Banking at its most interesting and beneficial right now, since. the information it unlocks is incredibly rich and useful.

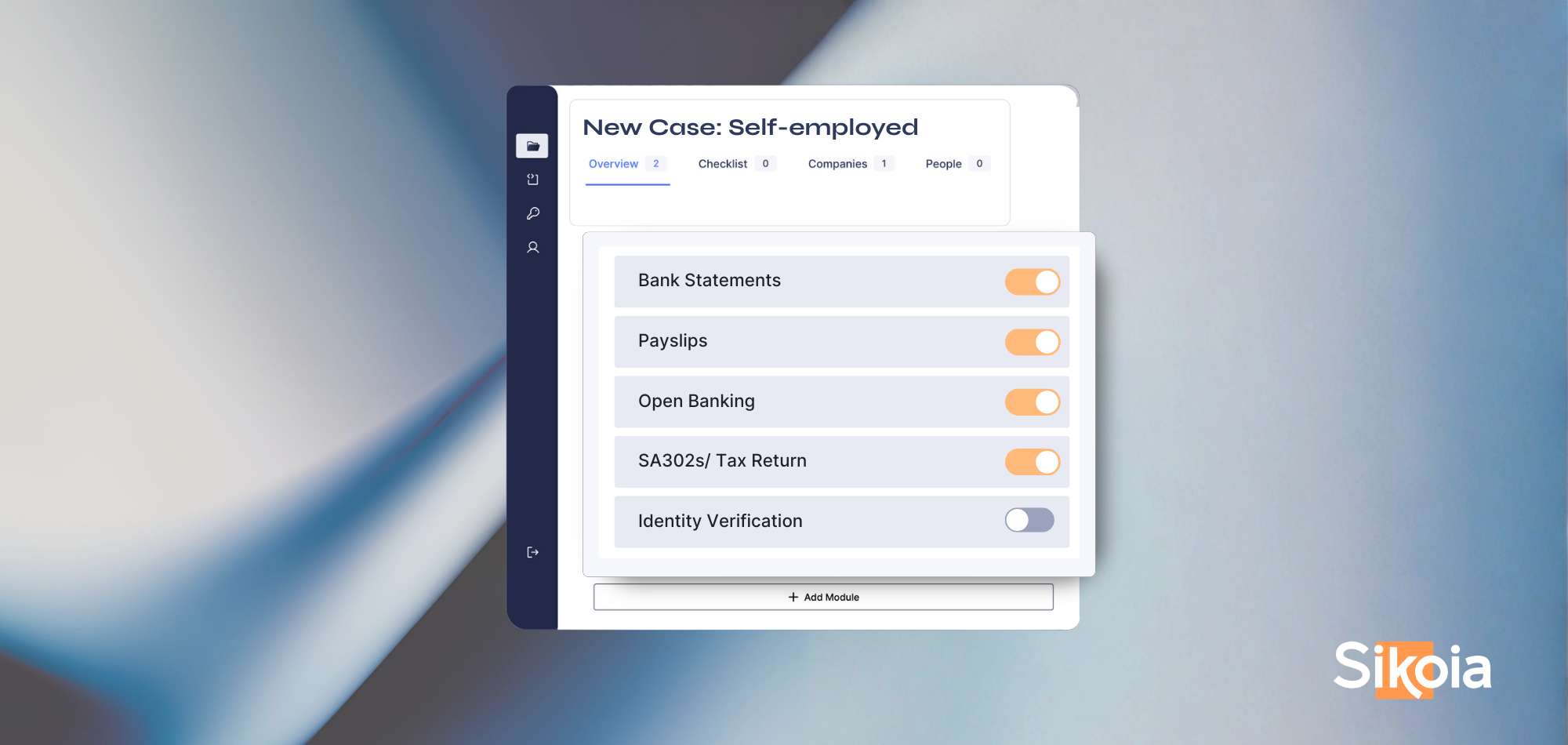

Open Banking can enable access to both account and transaction data. That information is valuable across a variety of use cases directly, as well as being helpful in terms of verifying any information you may already possess. For example, transaction data can allow you to double-check salary or income details and assess whether people can afford certain products or services. Account data can be used to validate certain personal information too – further strengthening your onboarding and KYC processes.

“In 2020, Open Banking powered almost 6bn [Account Information Service] calls in the UK alone. Globally, Experian supported 3.5bn credit decisions.” -- Rolands Mesters, CEO, Nordigen ”

This is illustrative of why these new and emerging APIs are so powerful: they provide benefits to users as well as innovators. For users, Open Banking is a secure and convenient way of sharing data without having to go through the tiresome process of digging up old financial documents.

A silver bullet?

That said, it’s important to acknowledge that consumer uptake is not universal. Many consumers are still uncomfortable sharing “unrestricted” access to their bank transaction data. Arguably, Open Banking is a victim of its own success: the very richness of the data set that it provides can occasionally be somewhat alarming to the consumers themselves – especially if they feel that doing so only surfaces “negative indicators”.

It is not just consumer uptake levels that can provide barriers to companies looking to take advantage of these latest APIs: multiple factors limit the universality of any given capability or individual provider. In the case of Open Banking, not every country has the same level of market coverage as the UK, which is very much an international leader. In other categories, data or capability companies often do not have universal coverage or universal availability. Any reputable credit risk professional will tell you that more complex and larger-scale applications require integrating with multiple bureaus to ensure proper coverage and redundancy.

For anyone looking to implement these APIs, there are several angles to consider. Open Banking is an important capability to implement – but will you need several different providers to ensure sufficient market coverage in the future? And what can you offer consumers who cannot, or will not, use Open Banking? You’ll also find many data sources will be incomplete or geographically restricted. So, again, how can you manage all those integrations in a simple and scalable manner?

More to the point, the process of selecting, signing, and implementing any given source can be expensive, complex, and above all time-consuming. To do this just once may be enough, but to have a robust solution, where you can effectively guarantee the availability of the capability itself, can become overwhelming.

Swapping old challenges for new

There are fresh data sources and capabilities coming online every day that will unlock entirely new categories of products and services. For example, we expect to see the UK government make more information available online soon. For small businesses and the self-employed, being able to share important financial information (especially a tax summary) quickly and securely will help companies deliver better and more competitive financial products. In Germany, we’ve started working with a partner that allows consumers to digitally verify their identity and sign contracts using only their Government ID card. The point is that with all these new data sources and capabilities coming online, new products and services will follow.

For financial services companies, and for those looking to implement new products or enter new markets, the evolution and maturation of the API ecosystem has been transformative. It is now easier than ever to access everything that you need, from data to complex functionality. However, this just creates another problem: managing the entire ecosystem itself. It’s true that provider discovery, selection, implementation, and maintenance can be a headache in isolation. But when you consider the need to implement multiple providers in each category to match your requirements, the whole scenario can become overwhelming. And this is before you even consider how to effectively orchestrate all these sources to ensure consistency and efficiency across your decisioning funnels.

“Data management’ must include ‘data supplier management"

At Sikoia, we’ve been working with our customers and partners to help solve these problems. Whether you’re a well-established financial services provider, or a new entrant looking to take advantage of these emerging capabilities for the first time, the problem you face is the same: managing an entire ecosystem of providers, including failovers and backups. There are several elements that have an important role to play – not least, being able to have a single actionable data layer and the means of orchestrating each individual source – and ideally a single point of access to the ecosystem to ensure consistency throughout. Without all of these, any attempt to manage your customers’ financial data will rapidly become overwhelming, and the value of these innovations will be eroded. But for those who have got it right, the benefits are enormous.

.png)

.png)

.png)

.png)

.png)

%20(2).svg)