Business customer due diligence processes – more frequently known as "know-your-business" (KYB) processes – play a crucial role for financial services providers and regulated companies, ensuring regulatory compliance, fraud prevention, and effective risk management in those business relationships. However, KYB processes are recognised for their inherent complexity and time-consuming nature. Companies often face a choice in how they approach this: either automate the process with predefined configurations or opt for a manual approach that offers greater flexibility.

Recent fintech innovations have an important role to play in providing more capabilities more easily, but are often point solutions. To orchestrate and manage all of these effectively requires a unified approach – specifically, a Unified Data Platform (UDP). A UDP combines the best of both worlds, blending automation capabilities with the flexibility required for efficient KYB processes.

In this post, we look at the different approaches to KYB processes and explain how leveraging a unified data platform can significantly enhance your processes.

Manual processes

Manual KYB processes involve a human reviewer who manually verifies the information provided by the business against various internal and external data sources and company policies. This approach is flexible, thorough, and precise; but tends to be more time-consuming and labour-intensive. The manual process typically includes the following steps:

- Collection of information: This information may include the business's name, address, tax ID number, and other relevant data obtained online or via vendors. If the company doesn’t have this information flow set up, they’ll need to identify and negotiate prices with vendors in the areas and jurisdictions that information is needed.

- Verification of information: Once the information is collected, the human reviewer will verify it against various data sources, such as official registers, public databases, and other sources of publicly available information.

- Assessment of risk: This includes analysing the business's industry, geographic location, and other factors that may increase the risk of fraud or non-compliance.

- Reporting and documentation: Finally, the reviewer will document the results of the KYB check and report any red flags or concerns to the business. The business may need to take further action to address any issues identified in the KYB check.

The key advantages to a manual process are:

- You are more likely to be able to make more decisions across a wider segment of your customer base, by going to non-standard data sources as needed.

- You can adjust to changing requirements – such as regulatory rules or risk appetite adjustments – more readily.

- Exceptions and expansions can be handled more easily.

The main drawbacks though are:

- It typically takes longer to complete an assessment, which often leads to a poor customer experience.

- Similarly, it may be hard to track and report on decisions – both at onboarding and during monitoring.

- Inconsistencies across assessments can arise when different team members assess customers differently or when there are no standardised guidelines.

Build an automated process internally

Building your own in-house automated solution is another viable approach, especially in higher-volume scenarios or scenarios where time-to-decision is a key metric. This option requires significant investment in time and resources to develop, maintain, and update the solution. The building automation internally process typically includes the following steps:

- Identification of requirements: This includes determining the data sources to be used, the types of verification checks to be performed, and the level of risk to be assessed. Similar with the manual process, if the company doesn’t have this information flow set up, they’ll need to identify and negotiate prices with vendors in the areas and jurisdictions that information is needed.

- Development of the solution: This involves designing the system architecture, developing the software, and testing the solution to ensure it meets the requirements.

- Implementation and deployment: This involve integrating the solution into the business's existing systems and workflows, training employees to use the new system, and ensuring that the system is working correctly.

- Maintenance and updates: Once the system is implemented, it requires ongoing maintenance and updates to ensure it remains effective and up to date with the latest regulations and data sources.

Again, there are a several advantages to doing this:

- You can make decisions – especially “happy path” decisions – more quickly, leading to a better customer experience.

- It’s typically easier to track and report on decision outcomes.

- You can remove bias and ensure adherence to your policy requirements.

But conversely, some drawbacks include:

- Adjusting to changes in the regulatory environment, your policy requirements, or even your vendor mix, is not straightforward.

- Dealing with atypical customers will almost certainly require manual intervention, especially in more complicated scenarios.

- You end up needing to dedicate valuable engineering resources to “back office” capabilities, rather than have them focus on your critical differentiators.

Buy an automated process

It’s possible to avoid some of these drawbacks by buying an automated process instead. Of course, buying an automated solution will certainly accelerate your time-to-market and allow you to make “happy path” decisions more quickly. However, an automated solution won’t necessarily improve how you manage more complex decisions – and often brings with it other restrictions, especially when it comes to expanding your coverage or adjusting your policies. Ultimately, these bottlenecks are as much on the data layer as they are on the technology layer.

This is where a unified approach to data comes in – and why more and more business are turning to a unified data platform (UDP). With a unified approach to data and comprehensive vendor coverage, a UDP is designed to allow you to address these limitations, whilst giving you the full suite of automation capabilities to support your risk assessment processes.

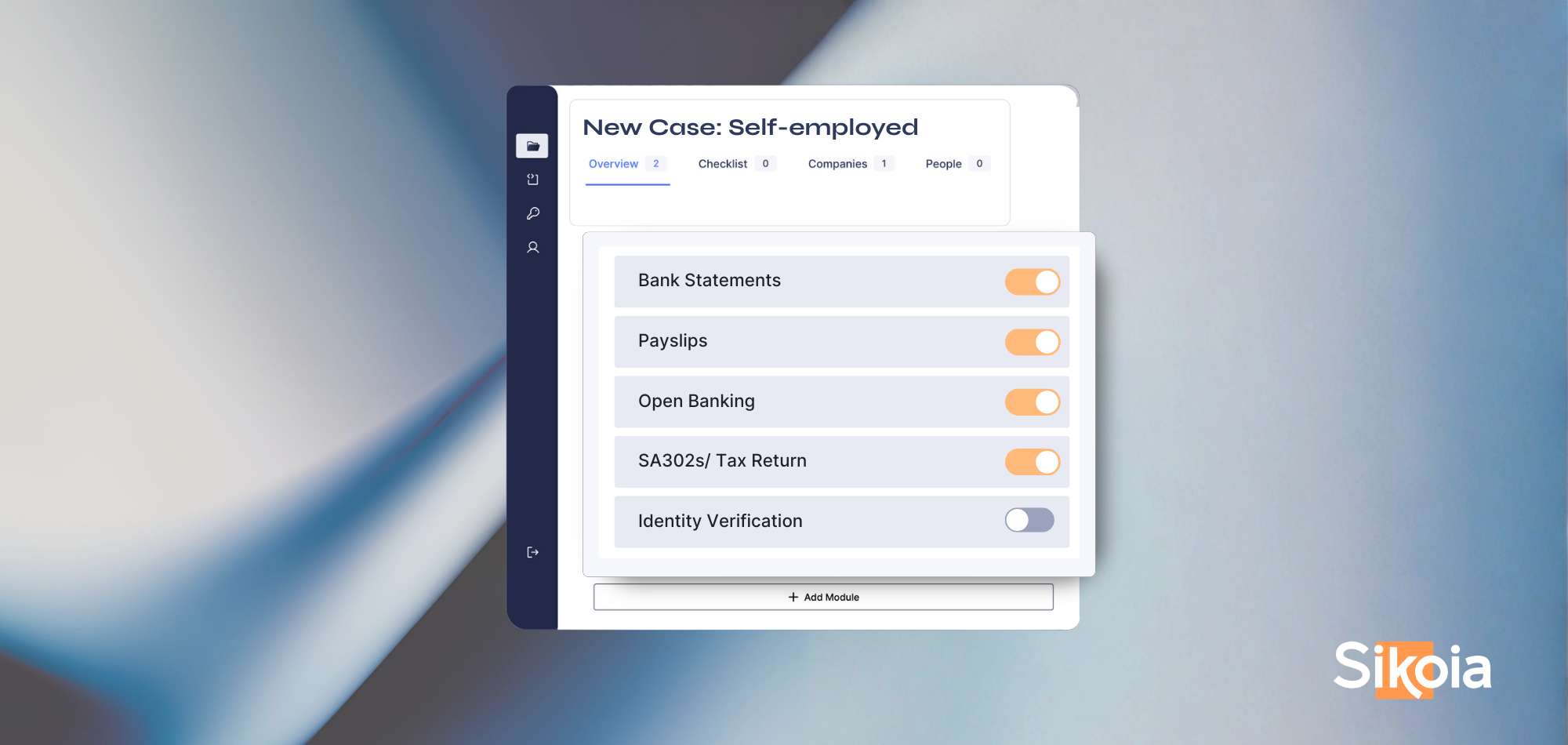

In the context of a KYB process, a UDP supports fully-automated company verification, AML screening, ID verification, AML risk scoring, and fraud checks on emails, phone, and bank details. With all the data you may need available through a standardised format, it’s also easier than ever to make decisions on more complex cases, more quickly – and keep track of how those decisions were made.

A unified data platform such as Sikoia can provide businesses a cost-effective solution that meets their KYB needs while minimising the amount of work needed from the company – especially as requirements evolve.

How to choose

When deciding on the approach that best meets your business's needs, you should consider the level of risk associated with your customers and the amount of time and resources you have available. The hybrid approach can provide a balance between efficiency and accuracy, while automation can offer businesses a cost-effective solution. Companies that decide to build automation internally must consider the cost and resources required, as well as compliance with regulations. Finally, a company like Sikoia offers a comprehensive KYB solution that ensures regulatory compliance, fraud prevention, and seamless onboarding.

The bottom line is, good KYB minimises onboarding friction by requesting the least amount of information possible.

.png)

.png)

.png)

.png)

.png)

%20(2).svg)