The year 2023 is shaping up to be an eventful period for financial services providers as they face – to name but a few – heightened regulatory scrutiny, stricter lending standards, and rising consumer living costs amid inflationary pressures. The payments sector continues to evolve rapidly, with new payment technologies and increasing popularity of digital payments, bringing emerging risks and challenges that firms in the sector must address. Most notably, the launch of the Financial Conduct Authority’s (FCA’s) new Consumer Duty obligations later this year will transform the landscape for all financial services providers, whether that’s payments companies, lenders, and advisors.

Earlier this month, the FCA released a letter addressed to payment services and e-money firms specifically, highlighting the regulator's expectations regarding consumer protection, competition, and innovation in the payment services industry. In short, the FCA's priorities aim to promote a fair, transparent, and innovative payments industry that protects consumers and supports the wider economy.

According to the report, certain payment firms were found to have significant problems with their governance, leadership, and oversight. Some of them lack experienced personnel, appropriate controls, and due diligence. To avoid regulatory scrutiny, it is crucial that these issues are addressed by the firms, as good governance is essential.

The FCA emphasised the importance of maintaining a robust risk management framework, ensuring the safety and security of customer funds, and complying with anti-money laundering regulations. It highlighted that its 2022/2025 strategy aims to reduce and prevent financial crime.

The FCA's main priorities in preventing compromises to the integrity of the financial system are centred around two areas: money laundering and sanctions, and fraud.

- All firms subject to the UK's Money Laundering Regulations must have comprehensive and proportionate systems and controls in place to identify, assess, monitor, and manage money laundering risk. The FCA has identified common issues with financial crime systems and controls at PIs and EMIs, including failure to conduct adequate KYC/due diligence, insufficiently detailed policies and procedures, and inadequate risk assessments.

- Under fraud, the FCA has observed elevated fraud rates in some PIs and EMIs and is concerned that there could be a further increase as a result of the cost-of-living crisis. The FCA expects firms to take immediate action to protect their customers against the risk of fraud and to ensure that their firms are not being used to receive the proceeds of fraud.

The FCA clearly stated that they expect firms to review their internal risk appetite statements and policies and procedures, regularly review their fraud prevention systems and controls, and maintain appropriate customer due diligence controls. Including conducting regular reviews to assess their compliance with anti-money laundering obligations and sanctions requirements and work swiftly to remediate weaknesses identified.

With regulatory checks and needs constantly tightening regulated companies that take advantage of the latest financial and data innovation represents a huge business opportunity and will prove a key long-term competitive differentiator.

How can we help you?

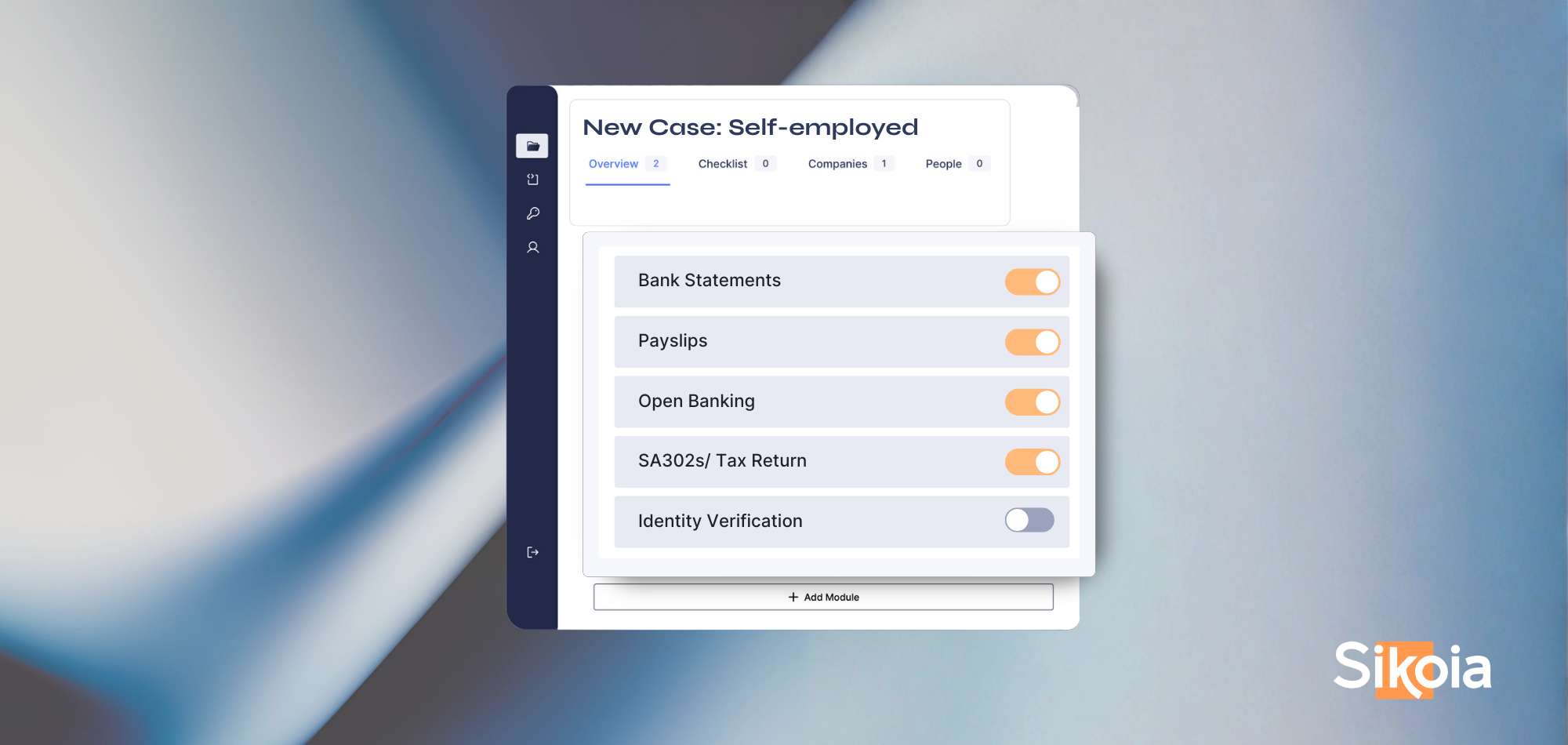

Sikoia’s Unified Data Platform allows financial service companies to conduct thorough customer due diligence – and support their reporting obligations in one single customer view with no need to negotiate multiple vendor contracts, all with its proprietary tech.

Sikoia’s Unified Data Platform Centralises client financial and identity data to simplify onboarding and verification, monitoring, and risk evaluation. Sikoia’s UDP includes access to a growing marketplace of international data partners and compliance services, including credit bureaus, public registries, identity verification, fraud screening, AML screening, and more.

.png)

.png)

.png)

.png)

.png)

%20(2).svg)