The gambling industry is arguably the single most regulated industry globally; and international companies especially must navigate a complex and constantly evolving regulatory environment across multiple jurisdictions to operate responsibly and sustainably. The recent fine of gambling company William Hill serves as a costly reminder of how important it is for gambling operators to comply with these regulatory requirements.

Knowing your customers

Failing to conduct proper due diligence and risk assessments can have serious legal, financial, and reputational consequences. For gambling operators, this can be quite complex, as many regulatory frameworks have requirements that exceed identity verification and AML screening (KYC checks) and touch on financial risk assessment and even affordability.

It is often challenging enough for many operators to simply maintain a robust level of customer due diligence for AML and affordability across their customers’ lifecycles, especially when juggling multiple vendors across multiple jurisdictions to satisfy specific requirements. However, any extensive and sufficiently robust process risks being both time-consuming and intrusive for the end customer, leading to many potential customers dropping off in the process. For operating companies, the key is maintaining robustness and a delightful customer experience.

The power of unified data

Considering the requirements above, any robust due diligence process will typically require the following:

- ID verification, and possibly confirmation of address/residency

- PEPs/Sanctions screening

- Liquidity and financial health checks, potentially using customer bank information

- Ongoing customer monitoring

Beyond this, there may be specific providers, or specific local requirements around each of the above in particular regions, introducing further complexity.

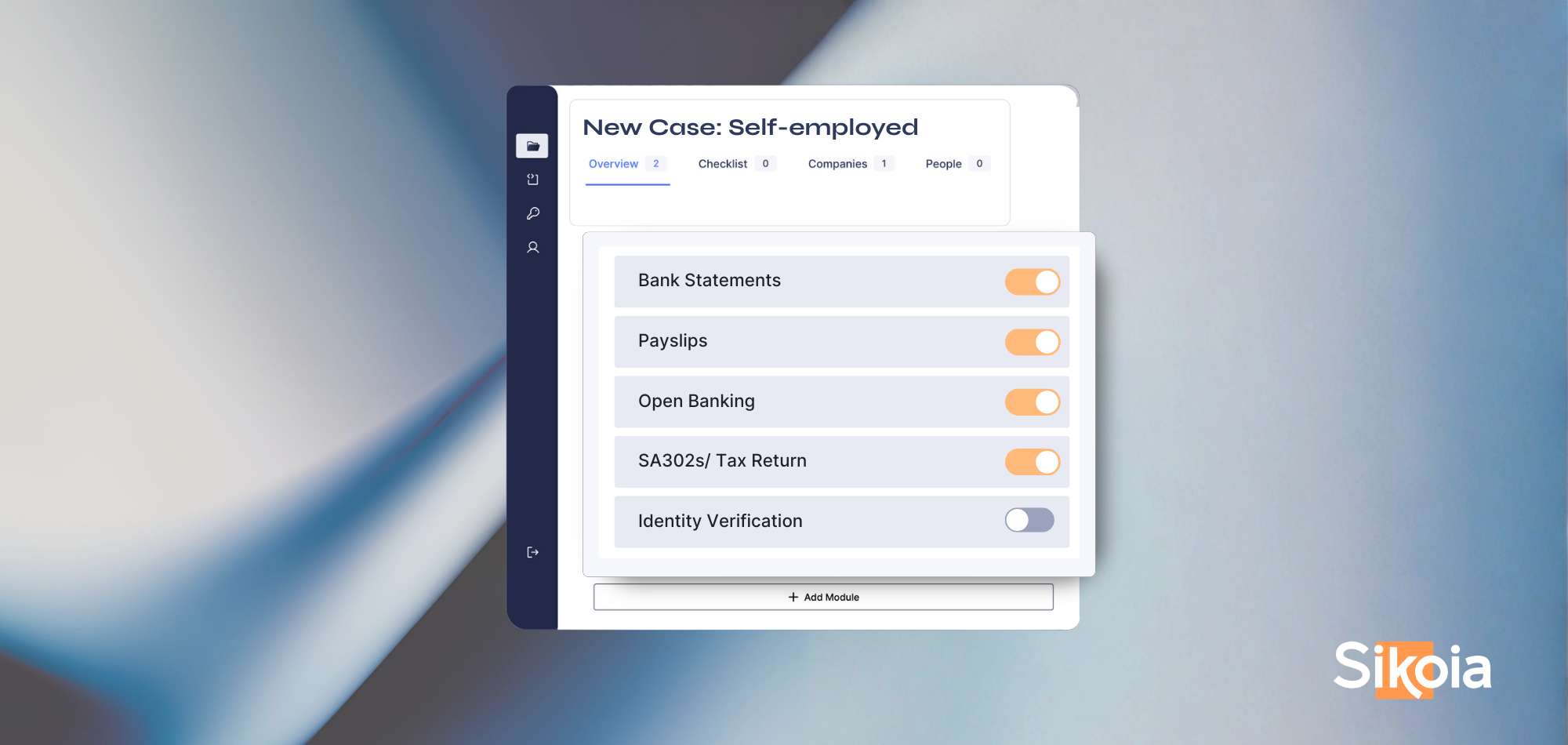

This is where a unified approach to data and data orchestration is particularly effective. A Unified Data Platform provides standardised access to each of the above capabilities – and more – across multiple point-solution providers in a consistent way. For example, in the Sikoia Unified Data Platform, we have integrations with multiple Open Banking providers to offer the best possible access across multiple regions, which we are extending with a proprietary bank statement ingestion pipeline to support affordability analyses in territories where Open Banking isn’t widespread. We even have integrations and capabilities to support payslip ingestion. These capabilities are all accessed consistently, removing data engineering complexity and provider maintenance and overhead; and the range of providers ensures we can deliver the broadest coverage possible for our clients.

More to the point, with a unified approach, gambling operators can realise measurable benefits from data cross-validations and synergies, and start building standardised and even automated processing flows. For example, it’s possible to develop sophisticated risk scoring models and surface meaningful flags and indicators across data “categories” – such as Open Banking data – without worrying about the details of the individual providers – such as Nordigen, Yapily, or Plaid. All of these can feed into custom data and analytics models, allowing operators to adopt best-practice risk-based approaches.

Accurate data today, compliant tomorrow

With both AML screening and reporting requirements tightening, and wider industry pressures to demonstrate consumer responsibility, gambling operators have a unique opportunity to set themselves up to be compliant over the longer term by building on the right capabilities today.

The hefty fine imposed on William Hill serves as a clear warning to all gambling operators to double-down on compliance. With a Unified Data Platform, operators can implement effective customer onboarding across the world, ensuring ongoing compliance and avoiding costly penalties.

About Sikoia

Sikoia is a category-defining Unified Data Platform (UDP) and orchestration layer that enriches and aggregates customer data from disparate sources and systems to automate compliance and risk processes, such as customer onboarding and verification, or portfolio monitoring. Client engagement and risk operations teams use the Sikoia Portal to access a fully-enriched, 360° view of the customer, and power operational efficiencies, delivering faster decisioning and powering best-in-class customer experiences.

.png)

.png)

.png)

.png)

.png)

%20(2).svg)